Introduction

The global trade system is broken. Current trade rules allow and even incentivize the perverse flow of capital away from where it is most needed and most productive toward the wealthiest parts of the world. Beyond depriving countries of much needed investment, the global trade system reflects broader problems that negatively impact consumers worldwide. By failing to recognize that industrial policy acts as a form of trade policy, current rules have perpetuated a system characterized by large, persistent, trade imbalances. Taking advantage of the free flow of capital, surplus countries subsidize their manufacturing industries but pass on the costs of these subsidies to deficit countries.

This has had important implications for U.S. manufacturing, unemployment, and debt. American assets are among the most attractive in the world. As a result, countries that subsidize their production via industrial and trade policy are acquiring American assets to balance their surplus and, in turn, the United States is running trade deficits. Because surplus countries have subsidized their manufacturing at the expense of domestic consumption, the U.S. manufacturing industry has been forced to indirectly subsidize American consumption. This has caused the decline of American manufacturing and a shift of global manufacturing from deficit countries to surplus countries over the past five decades.1 It has also depressed U.S. savings rates through a combination of higher unemployment, higher household debt, investment bubbles, and an ever-growing fiscal deficit, all caused by the influx of excess savings from surplus countries.

As one of the authors has discussed elsewhere, one of the consequences is apparent in global manufacturing data. In early 2024, Yao Yang, former dean at the National School of Development at Peking University, said on his blog that “America’s industrial base has already been hollowed out. How can it possibly compete [with China]? The United States has obviously made a strategic mistake.”2 He was right, but perhaps not for the reasons he thinks. While manufacturing comprises roughly 16 percent of global gross domestic product (GDP), according to the World Bank, the manufacturing share of China’s GDP is 28 percent, among the highest in the world, whereas for the United States it is 11 percent, among the lowest for any major economy.3 The opposite is true for consumption. While consumption accounts for 72 percent of global GDP, it accounts for 82 percent of the United States’ GDP and only 53 percent of China’s GDP.4

This means that although China comprises around 17 percent of global GDP, it accounts for around 29 percent of global manufacturing and 13 percent of global consumption.5 The United States, which accounts for 26 percent of global GDP, accounts for less than 16 percent of global manufacturing and nearly 26 percent of global consumption.6

While the differences in the two countries’ manufacturing and consumption shares of GDP may seem unrelated, they are in fact different expressions of the same imbalance. China and the United States are extreme representatives of a common pattern in the global economy. Manufacturing typically represents a disproportionately large share of the GDP of non-commodity economies with large, persistent surpluses, and consumption a low share of the GDP of such economies. The reverse is true for advanced economies that run large, persistent deficits.7

There is a cost to this imbalance. Consumers in surplus countries, individuals in countries with high investment needs, the American middle class, and American manufacturers, laborers, farmers, and producers all pay the price of this status quo. By targeting specific trade violations rather than balanced flows, trade policy has been focusing on the wrong outcome and creating a trade system that stifles the promise of global trade as a result.

To shore up American manufacturing, rein in debt, and generate higher-paying employment, the United States must either lead a transformation of the global trading system or force a change by unilaterally opting out of its current role. This would benefit the working class in both the United States and abroad by eliminating the persistent downward pressure on global demand created by surplus countries.

This will not be easy. A meaningful realignment of global trade imbalances will end—or at a minimum diminish—global dollar supremacy, and it will be strongly opposed by surplus countries. However, the true potential for trade to serve as a tool of mutual benefit and lift the fortunes of tens of millions cannot be unlocked without a change in the terms of global trade. New trade rules are needed to create an international trading system that preserves the United States’ freedom to set its own economic policy, protects the United States from bearing the costs of other nations’ industrial policies, and allows for the allocation of resources and production through a system of comparative advantage.

Subsidies in the International Trade System

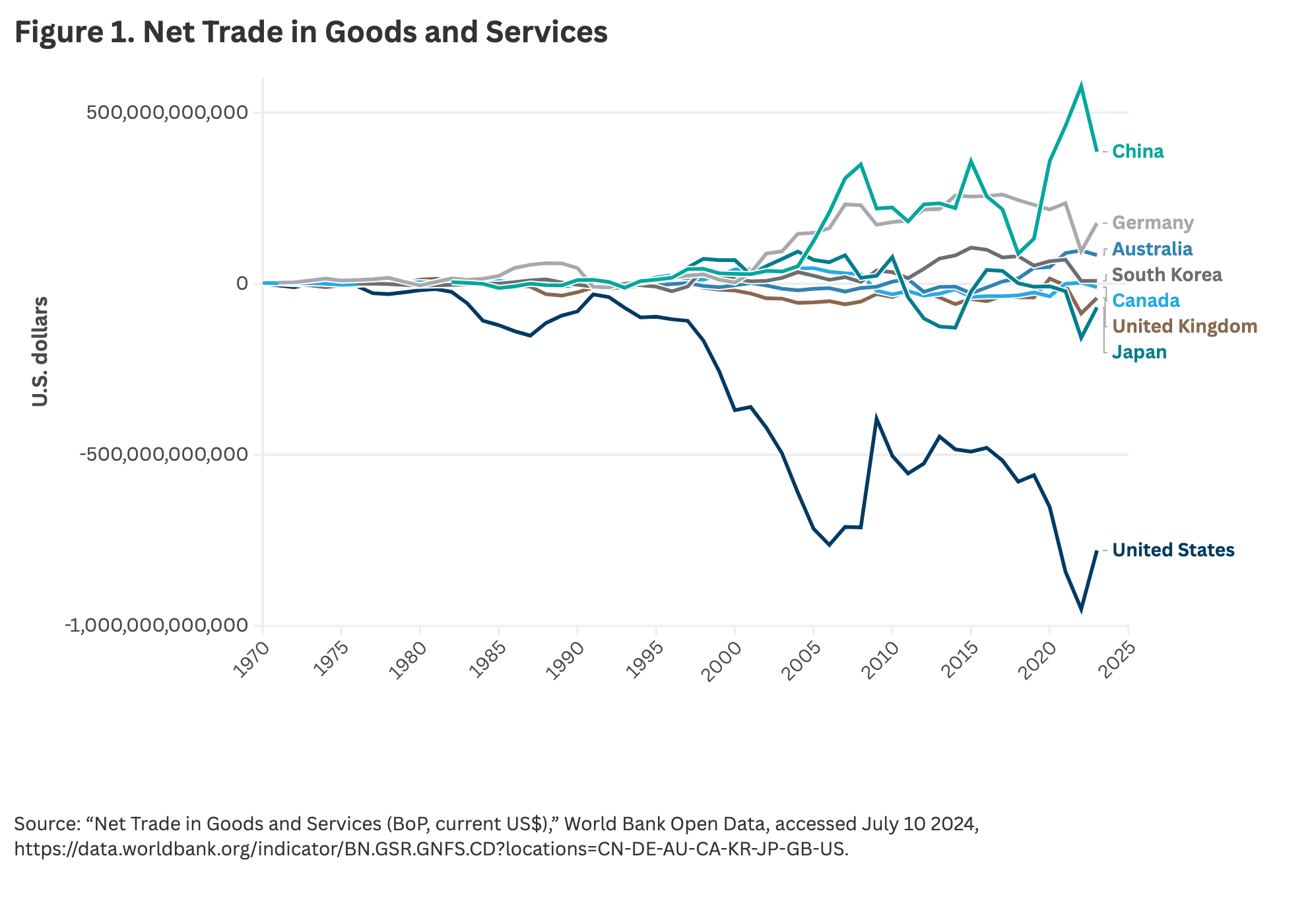

In the current international trading regime, some countries, such as the United States and the United Kingdom, consistently import more than they export, while others, such as China and Germany, consistently export more than they import. Figure 1 shows the trade balance for each of these countries, which measures the value of net exports in goods and services. The United States has persistently been a net importer, while certain other countries have persistently been net exporters.

Conventional economists argue that this pattern is due to comparative advantage, where countries with persistent trade surpluses hold the surplus because they have large manufacturing sectors, and their manufacturing sectors are large because these countries produce tradable goods more efficiently than deficit countries.8 But that is not how a true system of comparative advantage functions. Under comparative advantage, the purpose of trade is for each country to maximize domestic welfare by maximizing the value of imports, which in turn means maximizing the value of exports used to purchase those imports.

This does not imply that some countries are exporting or surplus countries while other countries are importing or deficit countries. Rather, it means that each country exports the goods and services in which it has a comparative production advantage in order to pay for imports of the goods and services in which it has a comparative disadvantage. In such a regime, trade must be broadly balanced, as countries exchange goods and services produced in their respective areas of comparative advantage for goods and services in which they are at a comparative disadvantage.

However, the current trade regime does not allow comparative advantage to determine which economies specialize in what; each country’s true comparative advantage is obscured by distortionary subsidies from the demand side of the economy. In surplus countries, industrial and trade policies force households to subsidize the manufacturing sector, giving the manufacturing sectors in these countries a competitive advantage against the manufacturing sectors of deficit countries. The suppression of labor costs, rather than increases in productivity, drives the distribution of manufacturing throughout the world.

There are a number of mechanisms through which surplus countries subsidize manufacturing at the expense of domestic consumption. Typical analyses of trade conflicts focus on direct subsidies, obscuring how indirect subsidies shape the contemporary global trade system. Manufacturing subsidies in surplus countries are often made possible through indirect transfers from households, which leave these households less able to purchase what these sectors produce, but bolster production. These transfers take a number of forms. For example, surplus economies typically have undervalued currencies as part of their trade strategies. Having an undervalued currency subsidizes manufacturing at the expense of households because households are all net importers—as they do not produce for the purpose of exporting—while net exporters are mostly manufacturers. An undervalued currency makes the manufacturing sector in that country more competitive, while reducing households’ consumption capacity.

The undervaluation of currencies is not the only, or most important mechanism through which transfers between consumers and producers shape the dynamic of global trade. Table 1 presents a list of additional noteworthy forms of transfer. For example, repression of interest rates below the neutral real interest rate has also been a powerful cause of financial transfers from household savers to manufacturers, as seen in Japan in the 1980s and China in the 2000.9 Further, overspending on transportation and infrastructure serves as an especially significant transfer from households to manufacturers in China today.10 Other transfers include centrally directed systems of credit, low penalties for environmental degradation, repressive labor laws, and restrictions on worker mobility.

| Table 1. Examples of Indirect Trade Subsidies in Surplus Countries and Their Effects | ||

| Form of Transfer | Effect on Consumers | Effect on Producers |

| Undervalued Currencies | Imports become more expensive, making consumption more expensive. This causes a real reduction in the household income share of GDP. | Exports become more competitive in the global market, increasing the manufacturing share of GDP. |

| Repressed Interest Rates | In economies in which households are largely net lenders, repressed interest rates force households to subsidize credit costs. | In surplus economies, net borrowers tend to be manufacturers and producers, who thus benefit from repressed interest rates. |

| Overspending or Inefficient Spending on Transportation and Infrastructure | The economic losses associated with overspending on nonproductive infrastructure are allocated across the economy, including to households. | Businesses and manufacturers benefit from better infrastructure and lower logistical and transportation costs. |

| Centrally Directed Credit | Credit risks are absorbed indirectly by households through low deposits rates. | Businesses can easily enter into new and risky businesses and ventures. |

| Low Penalties for Environmental Degradation | Environmental degradation raises health and absentee costs for workers and households. | Manufacturers benefit from reduced costs. |

| Repressive Labor Laws | Repressive laws reduce labor power, making it harder to keep wage growth in line with productivity growth. | Manufacturers benefit from reduced labor costs. |

| Worker Mobility Restrictions (for example, China’s Hukou System)a | Restrictions increase costs for migrant workers by depriving them of local social benefits. | Businesses indirectly benefit from reduced labor costs as a result of reduced social welfare costs. |

a The Hukou is a system of household registration, under which a person is identified as a resident of an area. An individual's Hukou registration determines their eligibility for many social benefits. Migrant workers face difficulties in changing their registration once they move, depriving them of benefits. For more on the Hukou system, see ”China’s Hukou Reform Remains a Major Challenge to Domestic Migrants in Cities,” Kam Wing Chan, World Bank Blogs, December 17, 2021, https://blogs.worldbank.org/en/peoplemove/chinas-hukou-reform-remains-major-challenge-domestic-migrants-cities. |

||

Such indirect transfers have the same effect as trade subsidies, yet are praised as successful forms of industrial policy rather than distortive trade interventions that hurt consumer welfare. An example of this is China’s subsidization of its electric vehicle (EV) industry, about which Gavekal analyst Yanmei Xie noted in a recent Financial Times article, “China’s well-rehearsed industrial policy can be staggeringly wasteful but still produce stunning results.”11

It is precisely because such subsidies are wasteful for the overall economy that they serve as both effective industrial policies and powerful trade interventions. These subsidies involve a transfer of wealth from Chinese household consumers to manufacturers, in the same way that import tariffs or undervalued currencies do, so that even if the overall productivity of the Chinese economy is compromised, the Chinese EV sector—and Chinese manufacturing in general—can maintain its international competitiveness. The costs are borne by households and not by other producers. What is more, as these subsidies leave the Chinese domestic consumer base too weak to absorb overall Chinese production, the cost of these subsidies must be externalized through large trade surpluses, forcing deficit countries to internalize the costs.

There is fierce debate about the extent of such subsidies globally. However, the presence of a simple set of conditions typically indicates the presence of subsidies. Economies that heavily subsidize manufacturers at the expense of households will typically have:

- larger manufacturing shares of GDP than their trade partners, since manufacturers must migrate to jurisdictions where workers are paid the lowest relative to their productivity to remain globally competitive in a hyper-globalized world;

- lower consumption shares of GDP than their trade partners, reflecting the cost of the subsidies on consumers;

- and large, persistent trade surpluses, as the repressed household income used to pay for manufacturing subsidies makes it impossible for domestic household consumption to balance trade.

When all three conditions hold, it is almost certain that repressed household demand is subsidizing manufacturing. And, indeed, we see this reduction of household consumption and increase in trade reflected in economic data for surplus countries (and the opposite trend for deficit countries). As shown in Table 2, over the past decade or so manufacturing has comprised roughly 16 percent and consumption 73 percent of global GDP. Against that average, the manufacturing share of China’s GDP has been roughly 28 percent, among the highest in the world, while consumption has only accounted for 54 percent. This reflects how China dampens domestic demand to boost Chinese manufacturing. By contrast, manufacturing has made up only 11 percent of American GDP, while consumption has made up 82 percent. In an inverse of the Chinese case, American domestic consumption is subsidized by the American manufacturing sector.

| Table 2. Manufacturing and Consumption as Shares of GDP | |||

| Average Manufacturing Share of GDP (2012–2022, %) | Average Consumption Share of GDP (2012–2022, %) | Trade Balance Historically | |

| United States | 11.00 | 82.00 | Deficit |

| Japan | 20.00 | 76.00 | Deficit |

| United Kingdom | 9.00 | 83.00 | Deficit |

| Canada | 10.00 | 78.00 | Deficit |

| World | 16.00 | 73.00 | N/A |

| South Korea | 26.00 | 65.00 | Surplus |

| Germany | 20.00 | 73.00 | Surplus |

| China | 28.00 | 54.00 | Surplus |

Notes: Countries are in ascending order based off a simple average of their trade balance from 2012 to 2022. Countries are coded as either historically deficit or surplus countries based on their trade balances over the 2012–2022 period. Canada and the United States are missing manufacturing share data for 2021–2022 and 2022, respectively, so the averages for those countries are taken over the truncated time period. Source: Author calculations using World Bank data: “Manufacturing Value Added (% of GDP),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NV.IND.MANF.ZS; “Final Consumption Expenditure (% of GDP),” World Bank Open Data, accessed July 10,2024, https://data.worldbank.org/indicator/NE.CON.TOTL.ZS?locations=CN-US; “Net Trade in Goods and Services (BoP, current US$),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/BN.GSR.GNFS.CD; “GDP (current US$),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NY.GDP.MKTP.CD; and “Final consumption expenditure (current US$),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NE.CON.TOTL.CD. | |||

We see this dynamic play out throughout the world. Among non-commodity economies with large persistent surpluses, manufacturing typically represents a disproportionately large share of GDP, while consumption takes up a disproportionally small share of GDP. The opposite is true for advanced economies that run large, persistent deficits, with relatively high consumption and low manufacturing.

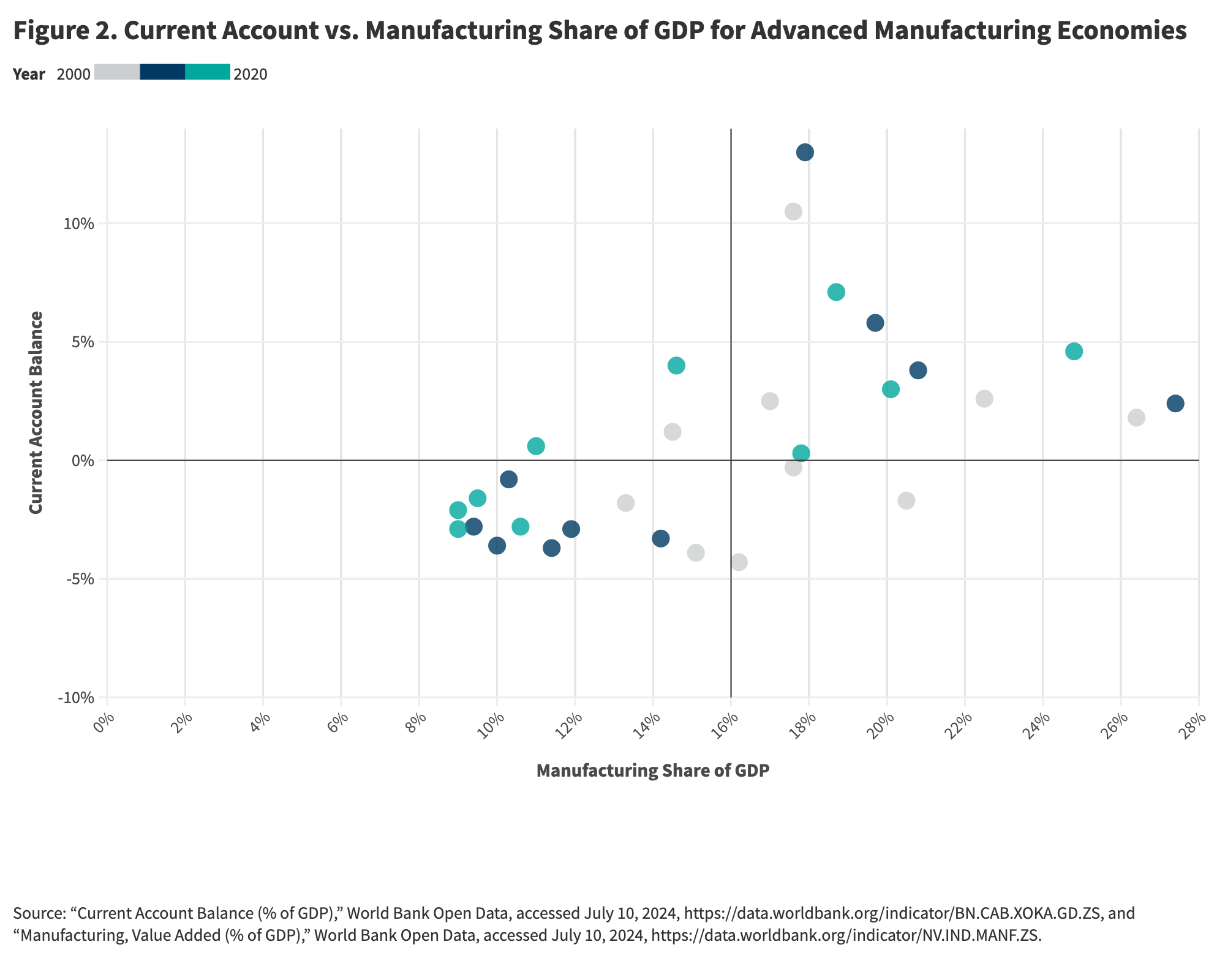

Under the current trading regime, manufacturing among advanced economies has shifted primarily to surplus countries. Figure 2 shows the relationship between the manufacturing share of GDP and the current account deficit for the ten-largest advanced economies in the world in 2000, 2010, and 2020 (explaining the thirty data points). As the scatterplot indicates, manufacturing shares of GDP are not always low for advanced economies. Rather, advanced economies with current account surpluses mostly have manufacturing shares of GDP that are above the global average (and populate the top right quadrant), while advanced economies with current account deficits have manufacturing shares of GDP that are below the global average (and populate the bottom left quadrant).

Japan’s history provides an illustrative example of the relationship between trade balances and manufacturing. In the 1980s and the early 1990s, when Japan ran the world’s largest trade surpluses, manufacturing averaged between 25 and 27 percent of its GDP, among the highest shares of any advanced economy.12 With the end of the Japanese asset bubble in the early 1990s, its trade surplus began to decline, and as it did, so did the role manufacturing played in Japan’s overall GDP. In the past five to ten years, as Japan has begun running trade deficits, manufacturing has come to comprise only 19 percent of its GDP.13

The shift in global manufacturing from deficit to surplus countries, then, is not the result of surplus countries holding a comparative advantage in manufacturing. It is the result of manufacturers responding to the direction of subsidies. What is at play in the current trading regime is not comparative advantage but rather transfers that distort comparative advantage and subsidize manufacturers at the expense of consumers in surplus countries.

These subsidies leave domestic consumers in surplus countries unable to absorb domestic production. This has turned the global trading system into one in which the purpose of exports is not to maximize the value of imports, but instead to externalize the consequences of suppressed domestic demand. Deficit countries are paying the price of suppressed domestic demand in surplus countries.

This repressed demand leads to high savings rates in deficit countries. Surplus countries such as China, Germany, and South Korea have higher average savings rates than the world at large and compared with deficit countries such as the United States and United Kingdom (see Table 3). There is a misperception that countries with high savings rates have households that value hard work and thrift;14 this is not true—rather, high savings rates result from the distribution of income across sectors of the economy.

| Table 3. Savings Rates and Household Consumption | |||

| Average Gross Savings Rate as a Share of GDP (2012–2022, %) | Average Household Consumption as a Share of GDP (2012–2022, %) | Trade Balance Historically | |

| United States | 19.00 | 68.00 | Deficit |

| Japan | 28.00 | 56.00 | Deficit |

| United Kingdom | 14.00 | 63.00 | Deficit |

| Canada | 21.00 | 57.00 | Deficit |

| World | 26.00 | 56.00 | N/A |

| South Korea | 36.00 | 48.00 | Surplus |

| Germany | 29.00 | 52.00 | Surplus |

| China | 46.00 | 38.00 | Surplus |

|

Note: Countries are in ascending order based off a simple average of their trade balance from 2012 to 2022. Averages were calculated using a simple average. Countries are coded as either historically deficit or surplus countries based on their trade balance over the period 2012–2022. Source: Author calculations using World Bank data: “Gross Savings (% of GDP),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NY.GNS.ICTR.ZS; “Household and NPISHs Final Consumption Expenditure (% of GDP),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NE.CON.PRVT.ZS; “Net Trade in Goods and Services (BoP, cur-rent US$),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/BN.GSR.GNFS.CD. |

|||

Ordinary households tend to consume a greater share of their income, while businesses consume none of their income, and governments and the extremely wealthy consume a low share of their income.15 In countries in which workers and ordinary households are unable to consume much of what they produce, the savings share of GDP (the portion of GDP that is not consumed) is by definition high. By contrast, when workers retain a greater share of their production, the savings rate is lower. Thus, repressed consumer demand due to indirect and direct transfers from consumers to manufacturers in surplus countries leads to lower savings rates in surplus countries, reflecting the inability of ordinary households in such countries to retain what they produce.16

When households cannot afford the goods and services they produce (in other words, when domestic savings exceed the amount of productive investment that can be absorbed by the economy), the economy has six options—none of them easy or pain-free.

The first is to raise household income to realign consumption and production by reversing subsidies. Such a realignment is very difficult, as it would impose a heavy economic cost on subsidized industries, undermining their current competitiveness. This is often a political nonstarter. Japan has been trying unsuccessfully to undo the subsidies that catapulted it to high-income status since 1986, and China has been attempting to do the same since 2007.17

A second option is to boost domestic spending on property, infrastructure, and manufacturing, even if it is unnecessary. This will allow the economy to absorb excess savings for some time. This is what was done in the Soviet Union and Brazil in the late 1960s and the 1970s, in Japan in the 1980s, and in China in the past ten to fifteen years.18 Unproductive investments, however, can create surging debt burdens. Unrecognized losses from unproductive investments inflate asset prices. Debt issued to fund such investments using these excess savings will reflect the inflated asset value rather than the true value. As a result, this debt will be unsustainable—when asset prices deflate to reflect their true value, the debt will remain structured as if the asset was more productive, and thus more valuable than it is.

A third option is to reduce production and fire workers to reduce savings. This will lead to a decline in both consumption and production until they are back in line. The United States adjusted in this way in the early 1930s through the Great Depression, and Brazil did something similar in the mid-1980s.19 However, this is an extremely painful form of adjustment that creates both negative growth and higher unemployment.

The fourth option is to lower interest rates to try to get households to raise their consumption through borrowing. But this avenue will eventually strain the household sector and is unsustainable. A fifth option is for the government to increase aggregate consumption through increased borrowing, but this too is unsustainable over the long term.

All five options are either politically painful, incomplete solutions, or both. As a result, many surplus countries choose the sixth option: externalizing the imbalance. Rather than rebalancing production and consumption domestically by ending subsidies, raising unemployment, or increasing debt, a country can run persistent trade surpluses, effectively exporting its excess savings—and the negative consequences of its subsidies—to its trade partners.

Effects on the United States

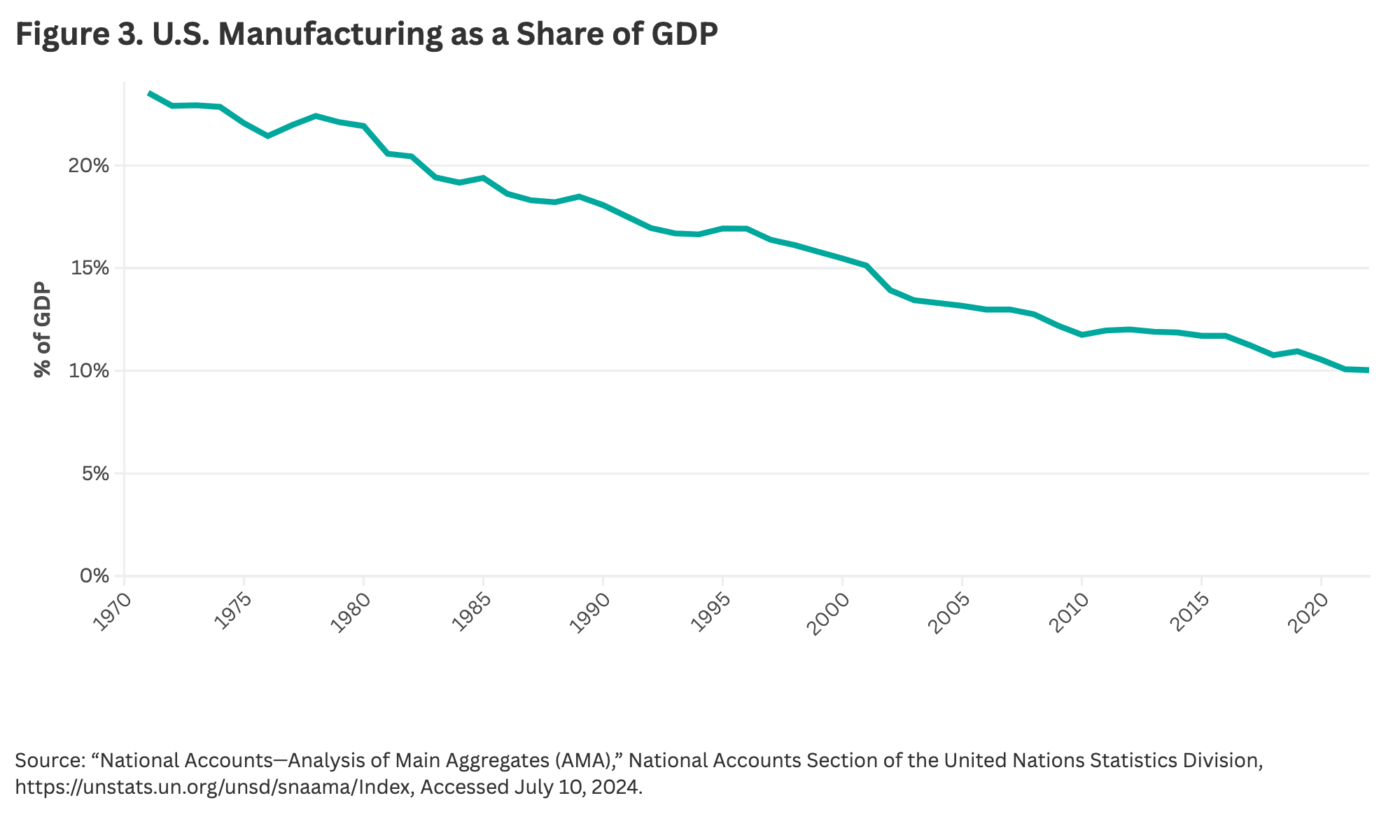

The United States, as a deficit country, experiences the opposite of what surplus countries experience. The current trade system increases the capacity of American households to consume, while reducing the competitiveness of American manufacturing. As a result, U.S. producers are effectively forced to subsidize U.S. consumers, which has hollowed out the American manufacturing industry. The U.S. share of global manufacturing fell from 15 percent to 10 percent over the period 2000 to 2021, as shown in Figure 3. Without the advantages foreign manufacturers enjoy due to their governments’ industrial policies, American manufacturers are forced to compete on unfair terms.

It is counterintuitive to think that it might not be a good thing to pay lower prices. However, just because American consumers pay lower sticker prices does not mean that the United States as a whole is receiving more for less as a result of surplus countries subsidizing their manufacturing sector. The current U.S. debate on Chinese EVs illustrates this confusion. Some commentators argue that China’s subsidization of EV production is good for the world because it makes it cheaper to buy EVs, while others argue that Chinese subsidies hurt the U.S. economy and slow the climate transition by making it more difficult for non-Chinese producers to compete.20

Although it is true that the sticker price for Chinese EVs is lower as a result of subsidization, this does not mean that it is ultimately China that bears the cost of this subsidy. Rather, because this surge in Chinese EV exports is not balanced by a surge in Chinese imports, U.S. producers are effectively funding these subsidies with lost income. These subsidies distort the production of EVs away from where it might be most efficient and may ultimately prevent EVs from being produced in a way that allows the world to collectively maximize its ability to produce goods needed for the climate transition.

Some economists argue that the decline in American manufacturing is not a problem, but rather a natural result of the development of the U.S. economy. They argue that the United States should deemphasize manufacturing in favor of other sectors, such as services and technology. However, the ability of other non-commodity advanced economies to maintain relatively high manufacturing shares of GDP disproves the idea that a decline in manufacturing is a natural, much less inevitable, result of economic advancement. For example, as shown in Table 2, while manufacturing represents on average 16 percent of global GDP, it represents 18 percent of German GDP and 26 percent of South Korean GDP. What unites these countries is that they have historically run trade surpluses by subsidizing their manufacturing sectors at the expense of their households. By contrast, manufacturing represents on average only 11 percent of GDP in the United States, 9 percent in Canada, and 8 percent in the United Kingdom, all historically deficit countries that have been forced to adjust to surplus countries’ industrial policies.

Thus, the decline in American manufacturing does not reflect comparative advantage but is rather a result of a global trade regime that distorts it by subjecting the U.S. economy to the impact of industrial policies chosen not by American policymakers but by the United States’ most aggressive trade partners. The decline of the U.S. share of global manufacturing is not caused by some natural evolution of the economy, but rather by the United States’ willingness to go along with this.

In addition to this decline in manufacturing, the U.S. is being forced to find a way to accommodate the glut of excess savings that surplus countries have exported to the United States. In principle, this adjustment could take the form of either increased investment within the U.S. or a decrease in domestic savings. Evidence suggests that the excess savings imported into the United States has not caused an increase in investment, suggesting instead that the inflow of excess capital has decreased domestic savings.

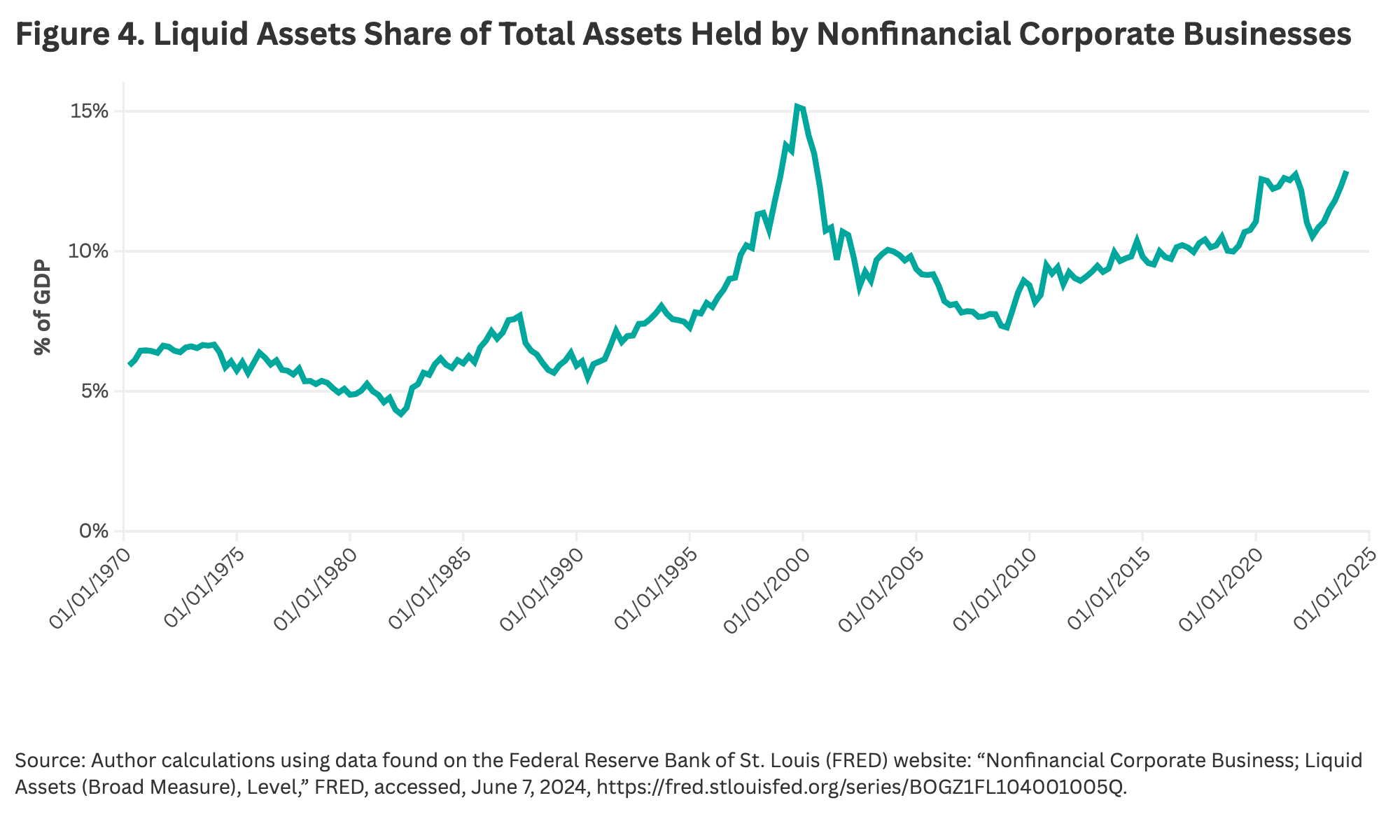

In the United States, business investment is not constrained by the scarcity of capital but primarily by demand. Indeed, American businesses sit on substantial piles of liquid assets, amounting to $6.9 trillion—approximately 12 percent of their assets, even after engaging in substantial acquisitions and share buybacks.21 Since 1970, the liquid asset share of total assets held by American businesses has risen sharply (see Figure 4). In such a context, in which investable capital is abundant, the economy is unable to absorb excess capital as productive investment. As a result, excess capital from abroad crowds out domestic savings. Thus, although the United States should in theory have a high savings rate (because the U.S. has a high level of income inequality and the rich save more of their income than the poor), the United States in fact has a low savings rate at 19 percent compared with 27 percent for the world.22

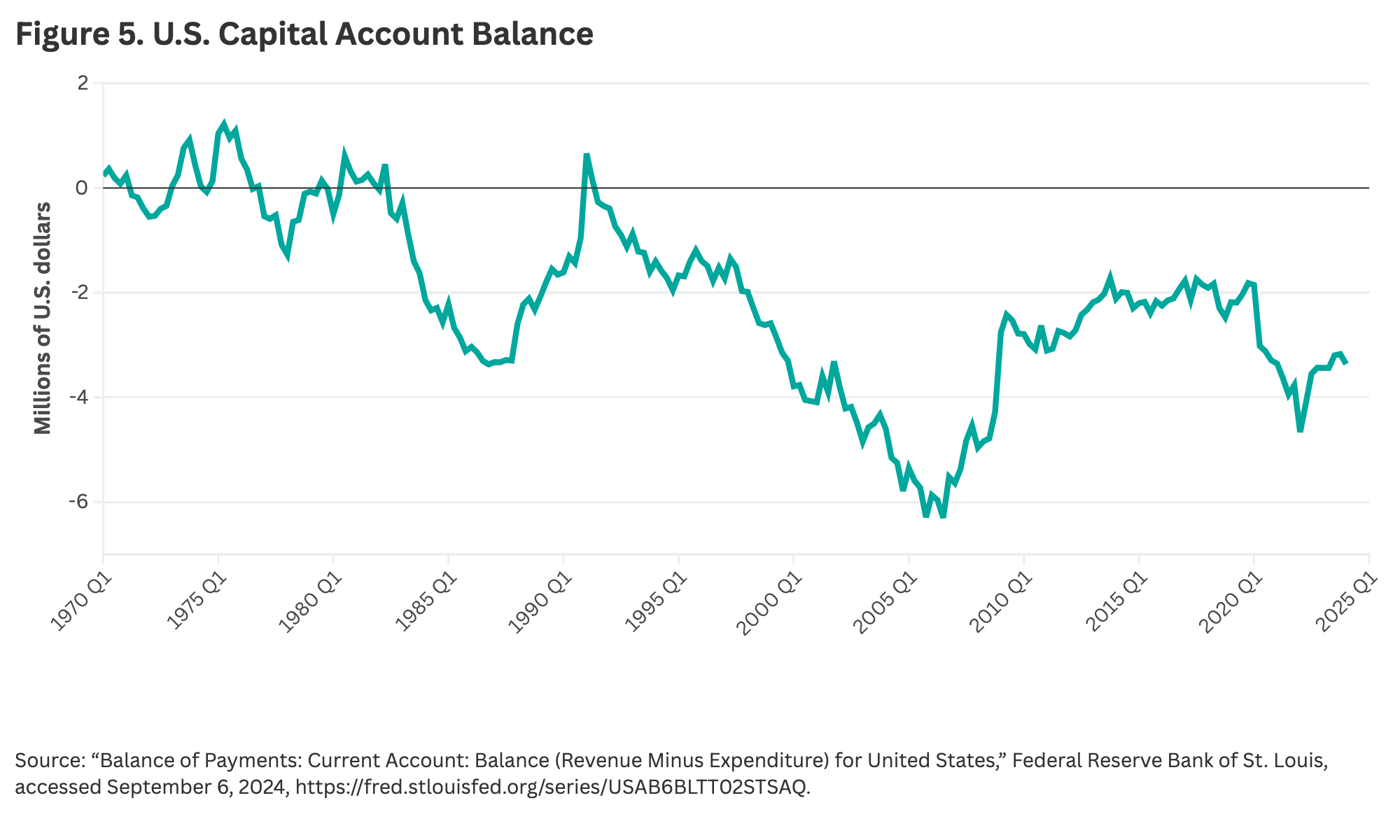

However, the United States has become the world’s top destination for excess global savings, because American assets, such as factories, farmland, apartments, and stocks and bonds, are highly valued abroad due to the United States’ flexible financial markets, robust corporate governance, and friendliness to foreign capital. As a result, much of the world’s trade surpluses have been externalized into the United States in exchange for assets. Because of this, and because the U.S. allows the free flow of capital into its borders, the United States has become a persistent net importer of foreign capital, pushing down its domestic savings rate. As seen in Figure 5, prior to around 1980, the U.S. capital account was roughly balanced, before turning deeply negative amid policy changes that allowed the free flow of capital into the country.

A number of mechanisms can cause foreign capital inflows to force down the U.S. savings rate. One of them is a rise in unemployment. As the emergence of a trade deficit forces U.S. imports to rise relative to exports, a portion of demand formerly directed toward domestic factories moves to foreign producers, without a compensating increase in demand from abroad for U.S.-produced goods and services. As a result, American producers are forced to lay off workers. Because workers must consume, regardless of their employment status, production falls faster than consumption, reducing the savings rate. Unemployed workers tend to have negative savings rates, as they must consume but typically have little to no income.23

However, most studies on the impacts of trade deficits on the U.S. economy do not attribute a substantial decline in employment to the rise of globalization.24 This is because the U.S. government has compensated for the reduced demand experienced by domestic producers through mechanisms that still force a reduction in American savings. Washington has typically done this through one of two ways: expanding the fiscal deficit or lowering interest rates.

In expanding the deficit, the U.S. government takes on more debt to raise demand in the economy, which lowers domestic savings, accommodating the inflow of foreign savings. When the Federal Reserve lowers interest rates, this expands the money supply, encouraging banks to expand household debt, which households can then use to expand consumption. Because this increase in demand is again fueled by debt, it reduces savings. The combination of lower interest rates and high foreign demand for U.S. assets can also create real estate or stock market bubbles, which further encourages household debt by forcing U.S. households to pay inflated prices for assets.

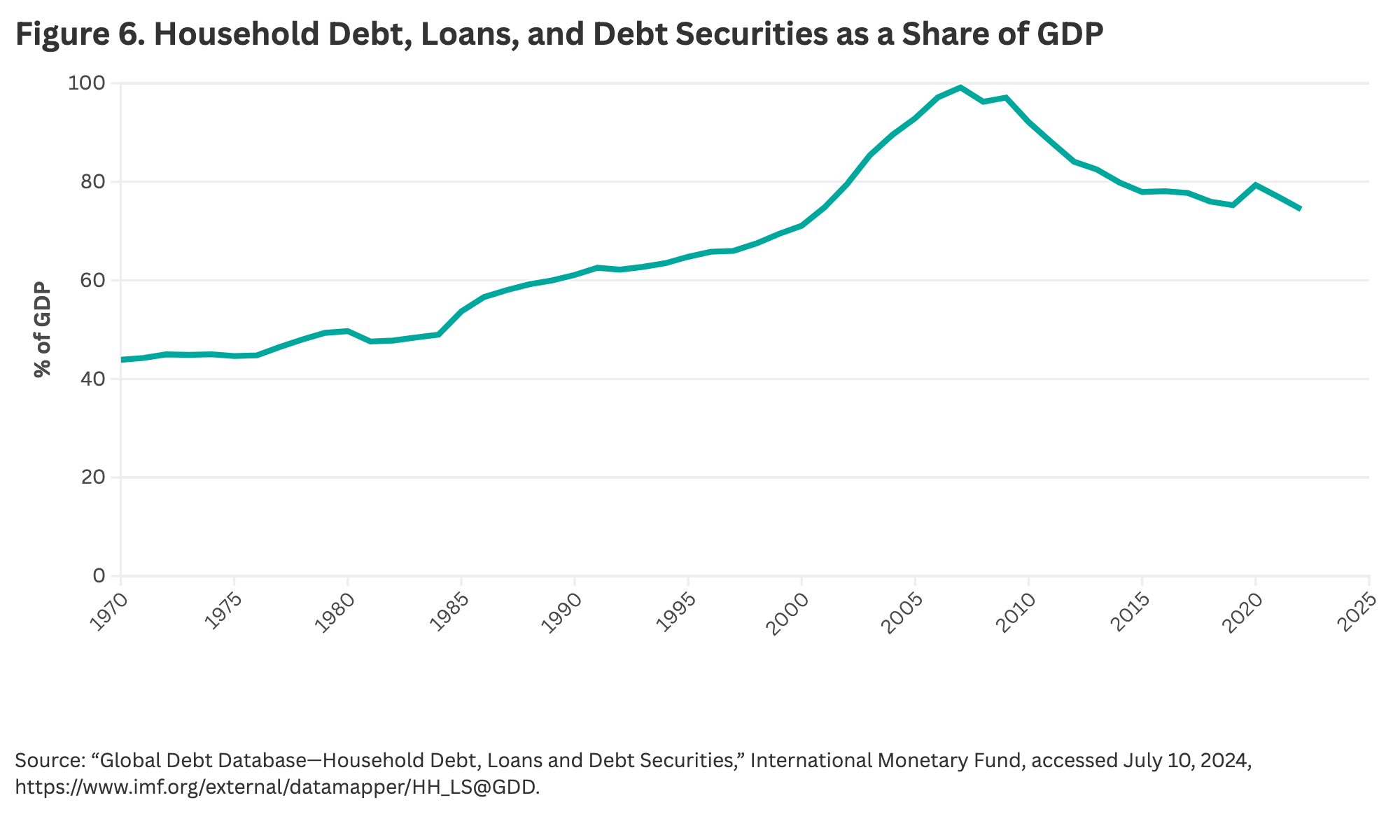

Data on the U.S. economy reflects this rise in government and household debt, as well as the accompanying fall in U.S. savings. The federal deficit has risen precipitously to over $1 trillion in 2023.25 The deficit has grown from 0.26 percent of GDP in 1970 to 6.2 percent in 2023, greater than the GDP share of the United States’ vaunted information sector in 2023.26 Data on U.S. household debt tells a similar story; the debt has risen from 43.9 percent of GDP in 1970 to 74.4 percent of GDP in 2022 (see Figure 6).

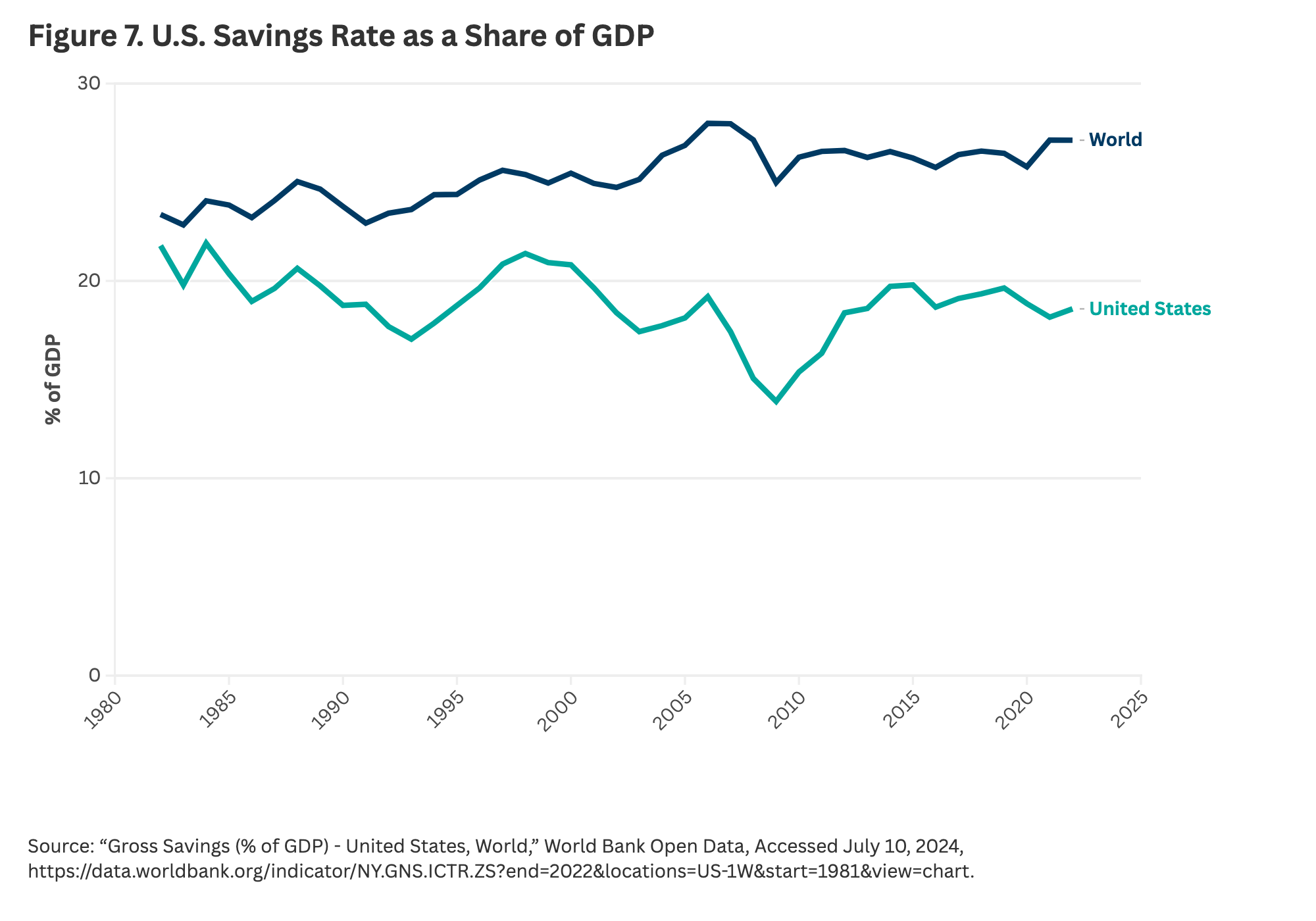

The consequence of this has been a decline in the United States’ savings rate relative to the global savings rate. As seen in Figure 7, forty years ago, the U.S. had a similar savings rate to the world as a whole (22 percent compared to 23 percent). Since then, however, a gap has opened. In 2022, the United States had a savings rate of 19 percent compared to 27 percent for the world.

Because the United States is unable to absorb capital inflows via a rise in investment, foreign inflows must cause a decline in savings, even if this does not occur through a rise in unemployment. As a result, the negative impacts of the current trade system do not show up in data through a rise in unemployment, but rather through a rise in debt and the erosion of the manufacturing share of the U.S. GDP.

Dollar Dominance, Capital Controls, and the Development of the Contemporary Trade Regime

The current global trading system, characterized by the dominance of the dollar and trade regulation that allows for persistent trade imbalances, was created through several important shifts throughout the course of the twentieth century.27 In the nineteenth century, trade was primarily funded through specie (gold and silver coins) and central banks held foreign currency on belief in the credibility of the issuing country’s commitment to converting that currency into specie.28 Thus, although in today’s economy, the dominance of the dollar results from the strength of the American economy, previously, a country’s relative economic might had nothing to do with a currency’s usefulness in trade. Although the U.S. economy had become the world’s largest by the end of the nineteenth century, the dollar remained relatively insignificant in global trade.29

Gold convertibility constrained trade in important ways. Under the pre-dollar system, trade imbalances were limited by the ability of each country to maintain convertibility. Each country’s currency was only useful in trade insofar as that currency could be converted for gold. Large trade imbalances threatened convertibility, as each country’s promise to exchange currency for gold became less credible when foreign holdings of the country’s currency rose relative to its central bank’s gold reserves. As a result, trade in the pre-dollar system was broadly balanced, with some small exceptions.

Gold convertibility also ensured that trade imbalances would self-correct through the price-specie flow mechanism. Surplus countries would experience an inflow in gold, raising the supply of money in surplus countries, which would then spark inflation; in response, exports from that country would decrease and imports would increase, as foreign products became more competitively priced. The opposite would occur in deficit countries, where the outflow of gold would spark deflation, making goods from the deficit country more attractive for export. Thus, demand contraction in deficit countries was always matched by demand expansion in surplus countries.30

This system shifted as Europe emerged from World War I with substantial reconstruction costs, much of which the victors sought to impose on Germany. This caused the dollar to rise, as the United States began exporting savings to fund reconstruction costs.31 Ultimately, however, this arrangement led to the 1931 European banking crisis and eventually both Germany and the United Kingdom abandoning the gold standard.32 Tensions over the inability of Germany and other debtor nations to repay the reparation and debts they owed following the war, the emergence of beggar-thy-neighbor policies, and a rise in isolationism, particularly in the United States, contributed to the Great Depression and the collapse of the international financial system.33

Following the end of World War II, the architects of the postwar economic system, convening at Bretton Woods, sought to apply lessons learned from the mistakes of post-World War I reconstruction. They strove to design a system that would prevent beggar-thy-neighbor policies and limit flows of speculative capital. However, they disagreed on how to do so.

British economist John Maynard Keynes argued for a global trading system in which surpluses and deficits could not persist. The American delegation, led by Harry Dexter White, rejected Keynes’s proposal, insisting instead on the establishment of an international fund to counteract destabilizing flows of capital. The resulting Bretton Woods system required countries to guarantee convertibility of their currencies to the dollar at a fixed rate, with the value of the dollar pegged to the value of gold (at $35 an ounce) and convertible to gold by foreign governments. 34 The International Monetary Fund was established to serve as the international fund White had envisioned, tasked with overseeing the system of fixed exchange rates.35

In 1971, U.S. president Richard Nixon devalued the dollar and halted the convertibility of the dollar to gold, ending the Bretton Woods system and ushering in a new era of unrestricted capital mobility. Following Nixon’s move, most of the world’s major currencies switched from fixed exchange rates to a free-floating system, so that the international flow of capital was no longer restricted by the need to maintain currency pegs. This combination of dollar dominance and unrestricted capital flows created the contemporary global trading system.36

What a Well-Functioning Global Trade Regime Looks Like

Advocates’ vision of globalization and unrestricted capital flows was to expand trade throughout the world, uninfluenced by market distortions, so that resources could shift to their most productive uses worldwide, enabling more people to consume more and increasing the economic fortunes of all.37 These advocates were correct in a way; if global trade can be structured to allow comparative advantage to determine the allocation of resources, more exports would automatically lead to more imports, and all parties would be better off through an expansion of trade.

However, the expansion of global trade unleashed after the demise of the Bretton Woods system did not occur within a context that facilitated the distribution of resources to their most productive uses. There are conditions under which an expansion of global trade must lead to either a contraction of global production, accompanied by a rise in global unemployment, or to ever increasing global debt, needed to bolster global demand.

Surpluses and deficits are not problematic in and of themselves. What matters is whether the excess of capital flowing from surplus to deficit countries is absorbed productively within the deficit country. If deficit countries can absorb this excess capital as investment, as would happen if investment in the deficit country was undersupplied, the global economy could become better off. However, if surpluses flow to places with no need for greater investment, the savings rate in the deficit country must fall to balance the inflow, either through a rise in unemployment or a rise in debt.

In any restructuring of the global trading regime, then, the rules of trade must ensure that resources are in fact able to flow where they are most productive. In a well-functioning trade regime, trade should be broadly balanced, ensuring that exports maximize imports. When trade imbalances do exist, they should mainly take the form of small, stable trade deficits run by rapidly growing low-income countries with investment needs that cannot be met by domestic savings and which instead meet those needs by importing savings from capital-rich advanced economies. Other forms of trade imbalances should be short-lived, since in a global economy without significant government-enforced distortions, surpluses and deficits will force fiscal and monetary changes that are automatically self-correcting.

Policy Solutions: Trade Interventions for Freer Trade

This world of balanced trade is not the world we live in. The current trade regime has been characterized for the past several decades by massive, persistent trade imbalances. Even more perversely, excess savings generated in both high- and low-income countries have mostly been directed to a handful of advanced, capital-rich economies, such as Australia, Canada, the United Kingdom, and the United States.

In the face of such a system, how should the United States respond? In recent years, policymakers in the United States have implemented countervailing industrial policies such as the CHIPS Act and the Inflation Reduction Act, seeking to counter the decline in American manufacturing and accompanying trade imbalances. Such policies could effectively encourage and protect specific manufacturing sectors, but if the United States persists in absorbing the excess savings of its trade partners, the country will continue to run a trade deficit and the American manufacturing sector as a whole will continue to decline. Thus, strategically important sectors of the economy may do well as a result of such policies, but only at the expense of the rest of U.S. manufacturing.38

Broadly speaking, deficit countries such as the United States have three options to respond to beggar-thy-neighbor policies: retaliate with similar policies of their own, aggressively subsidizing domestic manufacturing in the hopes of passing the cost on to their trading partners; accept the consequences of surplus countries’ policies, letting rising debt or unemployment set in and succumbing to the erosion of manufacturing in their economies; or opt out of the existing global trade regime, either unilaterally or with other like-minded countries, in the hopes of creating a new system that can truly unleash the potential of trade to raise global fortunes.39

The first option would lead to a crisis of global overproduction, unleashing economic calamity like that of the 1930s. The second option would likely be politically unacceptable within deficit countries over the long term, deepening the pain consumers have already experienced as a result of the current trade regime. In the case of the United States, it effectively amounts to the U.S. economy being subjected to industrial policy designed abroad—in China, Germany, Japan, South Korea, and other countries whose policies cause their economies to run persistent trade surpluses.40 The third option, meanwhile, would be deeply disruptive to global trade. Nevertheless, the third option is the right one for the United States. To move the world’s trading system toward one in which competitive advantage can truly determine the terms of trade, the best response for both the United States and the world in the medium and long term would be for the United States to intervene to reverse the beggar-thy-neighbor polices of surplus nations.

In this scenario, the United States, either unilaterally or with other like-minded countries, would implement policies that prevent surplus countries from externalizing the cost of their industrial policies by running persistent trade surpluses. This could be achieved either through restrictions on the ability of surplus countries to dump goods into the U.S. economy, for instance via the imposition of tariffs, or through restrictions on their ability to dump excess savings into the U.S. financial system, notably by taxing capital inflows.

Neither approach is a perfect antidote (see Table 4). A system of uniform tariffs, for instance, risks imposing the same costs on countries that are more and less aggressively mercantilist. Tariffs work to undo the U.S. trade deficit by forcing the rest of the world to reduce supply relative to demand, reducing the rest of the world’s excess savings. A uniform tariff on all imports does not discriminate between countries that run surpluses and those that do not. Also, more aggressive mercantilist countries will have a greater excess of savings compared with other countries, allowing them to better insulate themselves from the costs imposed by tariffs.

| Table 4. Comparing Policy Responses to Reduce Trade Deficits | |||

| Advantages | Disadvantages | ||

| Tariffs |

|

|

|

| Capital Controls |

|

|

|

Yet there are strategies to get around this problem. For instance, the United States could both build a broad consensus around reimagining the global trade system and address this problem of uniformity by making countries exempt from tariffs if they agree to join an agreement to implement similar “anti-mercantilist” tariffs. The United States could presumably wield tariffs more effectively and in a more targeted way, as part of a broader reorganization of trade aimed at creating new trade agreements that commit countries to maintaining broadly balanced trade.

For the United States, however, tariffs are a blunt instrument, limited in how they can be used to shift the balance of trade because of the country’s special role in the global economy. Tariffs can help to improve the competitiveness of American-made goods in the domestic market and dampen demand for goods made in surplus countries. That said, tariffs can only force a change in the excess of savings over investment in the rest of the world if they are set at such a high rate that they force a contraction of foreign production, followed eventually by an expansion of foreign demand.

Tariffs do not always achieve such a contraction. For example, when the United States set tariffs on Chinese imports in 2018, there was no effect on the U.S. current account deficit; the tariffs could not shift the balance between Chinese savings and investments, and China therefore continued to export its excess savings to the United States. Tariffs can shift the bilateral trade balance between a deficit and surplus country, but without a fundamental realignment in the surplus country’s savings and investments, neither side’s overall trade balances will shift. Bilateral tariffs, like those recently imposed against China by the administration of U.S. President Joe Biden, can strengthen particular manufacturing sectors that the United States considers strategically important, but they cannot drive a revival of global manufacturing overall or fix the core problem of beggar-thy-neighbor policies.

A more direct and focused alternative to tariffs is to reintroduce capital controls. So long as the United States allows unfettered access to purchases of American assets and it remains the preferred destination for excess savings from abroad, the United States will have no choice but to run a trade deficit. If the rest of the world chooses to implement industrial policies that suppress domestic demand and force up their savings relative to investment, as long as they can freely export these excess savings to the United States by buying American assets, the U.S. trade account and savings rates will be forced to accommodate these inflows, resulting in a persistent U.S. trade deficit. The United States could address this reality by adopting capital controls to prevent other countries from freely exporting excess savings into the United States. If the U.S. were to tax capital inflows, or otherwise control them, surplus countries could not externalize the costs of their excess savings into the United States.

Capital inflows could be controlled through a number of mechanisms, including taxes, volume restrictions, bank reserve requirements, government approvals for transactions, and limitations on investor eligibility. An effective capital inflow regulation regime would need to be flexible, allowing for benign, temporary trade imbalances that balance an increase in productive investment while penalizing short-term and speculative inflows.

A tax on foreign investment, such as that proposed in a bipartisan 2019 bill introduced by U.S. senators Tammy Baldwin (D-WI) and Josh Hawley (R-MO), would regulate capital inflows flexibly by penalizing short-term investments more than long-term investments and by tasking the Federal Reserve with shifting the tax rate on foreign investments to target a balanced current account.41 A flexible tax rate that shifts with the trade balance would allow for inflows when foreign investment would be productive, while also creating a tool to protect the United States from dumping and from destabilizing speculation. In addition to helping make the global trading system more productive, such a tax would improve financial stability and productivity and ultimately foster economic growth.42

Critics of taxing capital inflows and other means of restricting capital inflows argue that they would raise domestic interest rates. Maurice Obstfeld, an economist at the Peterson Institute for International Economics, argues that because restricting inflows from abroad would make borrowing foreign capital more expensive, the cost of borrowing in the United States would increase overall. He points to this supposed increase in the cost of borrowing to argue that restricting capital inflows would have an inflationary effect.43

However, investment in the United States is constrained by weak demand, not the scarcity of capital. Indeed, there is an oversupply of capital in the country, as shown in Figure 4. Domestic capital that is currently unproductive is readily available as an alternative to foreign capital should the cost of borrowing from abroad rise. Thus, foreign inflows are not currently lowering interest rates, and reducing the supply of foreign inflows would not in turn raise interest rates.

Significantly restricting capital inflows into the United States would substantially change the role that the dollar currently plays in the global economy. The U.S. dollar is the world’s most widely used currency because of the depth, liquidity, and flexibility of U.S. financial markets, along with the country’s strong protection of foreign investment. The dollar dominates global trade and capital flows because the United States acts as the most significant absorber of global excess savings. Preventing foreign actors from easily accessing American assets would reduce the global significance of the dollar and move the world toward one in which no currency plays the role that it currently plays.

The United States could control capital flows unilaterally, or with the world’s other major economies as part of a broader reimagining of the global trade and capital regime. A unilateral shift would likely be extremely painful and, in some cases, even destabilizing for countries such as China, Germany, Japan, Russia, and Saudi Arabia; these countries would likely be unable to quickly resolve domestic demand and savings imbalances. On the other hand, such a move would boost American manufacturing, raise domestic wages, and force U.S. businesses once again to rely on raising productivity rather than lowering wages to achieve international competitiveness.44

A multilateral shift toward a new trade and capital system, however, would be less disruptive for the global economy and allow the United States and other countries to maintain some degree of control over global trade and capital flows. Washington and its allies could do so by negotiating a new set of trade agreements that would force members to resolve their domestic demand imbalances at home rather than force their trade partners to absorb them. One mechanism to do so, originally proposed by Keynes at Bretton Woods would introduce an International Clearing Union and a global synthetic currency (which he called the bancor) designed to absorb global imbalances and spread out their consequences across the major economies.45

A shift toward capital controls would affect different American constituencies in unique ways. A more productively allocated global trade system, as well as the improved financial stability that would result from capital controls, would likely generate broad economic growth. American workers, farmers, and domestic producers in particular would benefit from the ability to engage in global trade fairly. However, three significant and powerful American constituencies will likely protest this shift away from dollar dominance: Wall Street, the foreign affairs establishment, and large corporations.

The American high finance industry is globally dominant because of the global dominance of the U.S. dollar in trade and capital flows. With the end of dollar dominance, American financial services firms could not capture such a large share of global profits. The foreign affairs establishment currently uses the dominance of the U.S. dollar to impose sanctions on countries that oppose U.S. geopolitical interests, prompting unfriendly nations such as China and Russia to explore de-dollarization on their own terms. Reducing the importance of the dollar in global transactions would take away sanctions as a policy lever. Finally, large multinational corporations benefit from the easy transfer of capital in and out of the United States, which allows firms to easily operate across borders and move resources toward jurisdictions in which they have a tax advantage.

American policymakers face a choice. Whose interests should they prioritize? By maintaining the status quo, they side with those powerful constituencies that benefit from dollar dominance. The move toward a new trade paradigm, on the other hand, could rein in the economically powerful to create a more equal economic system that unleashes renewed productivity, ensuring that trade works for all Americans.

Conclusion

Although there is a tendency in policy circles to treat industrial policy and trade policy as separate, there is no meaningful difference between most forms of the two. Because savings must equal investment across the entirety of the global economy, any policy that forces up the savings rate in one area must be balanced by either higher investment or lower savings elsewhere. As a result, any economic, monetary, or fiscal policy that affects the balance between a country’s domestic savings and its domestic investment must necessarily affect the country’s trade balance and, through its trade balance, affect the balance between the savings and investment of its trade partners. This is why in the current system countries are able to effectively impose trade policy onto one another through beggar-thy-neighbor industrial policies.

Trade restrictions, particularly capital controls, can restore the freedom of countries to direct their economic policy in favor of their citizens, and restore the world to a system of truly free trade, in which comparative advantage determines the distribution of resources. In this way, trade restrictions can lead to a world of freer trade.

There are a wide range of policies that cause trade distortions, many of which do not target trade explicitly. As a result, to create a global trade environment that can truly unleash the benefits of trade, the rules of the global trade system should target overall trade imbalances, as Keynes proposed at Bretton Woods, rather than target specific trade violations. Because the World Trade Organization and other trade regulatory bodies have focused on the latter, the current trade system continues to stifle the promise of global trade. That is why the United States, and most of the rest of the world, would be better off with a radical reorganization of the global trading system.

Acknowledgments

The authors are grateful to Stewart Patrick, Ann Pettifor, and Peter Harrell for their thoughtful and incisive feedback. They would also like to thank the Carnegie Communications team for their invaluable work throughout the publications process.

Notes

1Michael Pettis, “Trade and the Manufacturing Share,” Phenomenal World, June 28, 2024, https://www.phenomenalworld.org/analysis/trade-and-the-manufacturing-share/.

2Michael Pettis, “Can Trade Intervention Lead to Freer Trade?,” Carnegie Endowment for International Peace, February 23, 2024, https://carnegieendowment.org/china-financial-markets/2024/02/can-trade-intervention-lead-to-freer-trade?lang=en; and Amanda Lee, “In US-China Rivalry, Beijing Advisers Urge ‘Rational’ Approach During Election Year, but Will Pragmatism Win Out?,” myNews, January 20, 2024, https://www.scmp.com/economy/china-economy/article/3249130/us-china-rivalry-beijing-advisers-urge-rational-approach-during-election-year-will-pragmatism-win?utm_source=twitter&utm_campaign=3249130&utm_medium=share_widget.

3“Manufacturing Value Added (% of GDP),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NV.IND.MANF.ZS.

4“Final consumption expenditure (% of GDP),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NE.CON.TOTL.ZS?locations=CN-US; and author calculations using ”Final consumption expenditure (Current US$),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NE.CON.TOTL.CD and “GDP (current US$),” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/NY.GDP.MKTP.CD.

5Author calculations using “Final Consumption Expenditure (current US$),” World Bank Open Data, Accessed July 10, 2024, https://data.worldbank.org/indicator/NE.CON.TOTL.CD; “Manufacturing, Value Added (current US$),” World Bank Open Data, Accessed July 10, 2024, https://data.worldbank.org/indicator/NV.IND.MANF.CD; and “GDP (current US$),” World Bank Open Data, Accessed July 10, 2024, https://data.worldbank.org/indicator/NY.GDP.MKTP.CD.

6“World Bank Open Data.”

7The preceding three paragraphs were originally published in Pettis, “Can Trade Intervention Lead to Freer Trade?” The data has been updated to reflect information as available at time of drafting in September 2024.

8William Lastrapes, “An Economist Explains Why Trade Deficits Aren’t a Bad Thing,” World Economic Forum, October 16, 2018, https://www.weforum.org/agenda/2018/10/why-trade-deficits-aren-t-so-bad/.

9The discussion on “repressed interest rates” refers to situations in which monetary policy sets the interest rate below the neutral real interest rate (the interest rate at which monetary policy is neither expansionary nor contractionary), which would prevail when the economy is at full employment and inflation is stable. Low interest rates need not act as an indirect subsidy per se—what matters is the relative interest rate level rather than the absolute level. For the China example, see Shiting Ding, Yanming Zhang, Jingru Zhang, Qiong Yang, and Jindong Luan, “Study on the China’s Real Interest Rate After Including Housing Price Factor into CPI,” PLOS ONE 18, no. 8 (2023): e0290079, https://doi.org/10.1371/journal.pone.0290079.

10“China’s Infrastructure Spending Is Marred by Problems, Audits Show,” Bloomberg, September 6, 2023, https://www.bloomberg.com/news/articles/2023-09-06/china-s-infrastructure-spending-is-marred-by-problems-audits-show?embedded-checkout=true.

11Yanmei Xie, “China’s Cull of EV Overcapacity Will Bring Little Relief to Europe,” Financial Times, February 4, 2024, https://www.ft.com/content/608c4b00-8efb-4322-9318-f6249096e3fe?sharetype=blocked.

12“Japan—Manufacturing, Value Added (% Of GDP)—2024 Data 2025 Forecast 1980–2022 Historical,” Trading Economics, accessed July 10, 2024, https://tradingeconomics.com/japan/manufacturing-value-added-percent-of-gdp-wb-data.html; and Clyde Farnsworth, “Japan-U.S. Trade Gap $13.4 Billion,” New York Times, January 19, 1982, https://www.nytimes.com/1982/01/19/business/japan-us-trade-gap-13.4-billion.html.

13“Japan—Manufacturing, Value Added (% Of GDP)—2024 Data 2025 Forecast 1980–2022 Historical”; and “Net Trade in Goods and Services (BoP, current US$) - Japan,” World Bank Open Data, accessed July 10, 2024, https://data.worldbank.org/indicator/BN.GSR.GNFS.CD?locations=JP.

14Michael Pettis, “The U.S. Trade Deficit Isn’t Caused by Low American Savings,” Carnegie Endowment for International Peace, China Financial Markets, August 8, 2018, https://carnegieendowment.org/china-financial-markets/2018/08/the-us-trade-deficit-isnt-caused-by-low-american-savings?lang=en.

15Atif Mian, Ludwig Straub, and Amir Sufi, “The Saving Glut of the Rich,” National Bureau of Economic Research, February 2021, https://scholar.harvard.edu/files/straub/files/mss_richsavingglut.pdf.

16Michael Pettis, “China’s Problem Is Excess Savings, Not Too Much Capacity,” Financial Times, April 29, 2024, https://www.ft.com/content/879f5de7-cd9b-4987-9c2b-8b23cf0f3800.

17“IMF Survey: China’s Difficult Rebalancing Act,” International Monetary Fund, accessed July 10, 2024, https://www.imf.org/en/News/Articles/2015/09/28/04/53/socar0912a; “Attacking Japan’s Saving-Investment Imbalance: Structural Adjustment Versus Fiscal Stimulus,” Central Intelligence Agency, April 11, 1986, https://www.cia.gov/readingroom/docs/CIA-RDP86T01017R000605930001-7.pdf.

18Li Yuan, “China’s Cities are Buried in Debt, but They Keep Shoveling It On,” New York Times, March 28, 2023, https://www.nytimes.com/2023/03/28/business/china-local-finances-debt.html; and Richard Vague, “How Japan Lost Its Decade (and More),” Public Finance Focus, October 20, 2023, https://www.publicfinancefocus.org/depth/2023/10/how-japan-lost-its-decade-and-more.

19Antonio Jorge Fernandes, Margarete Arbugeri and Nilton Formiga, “The Brazilian Economy in the 1980s,” International Journal for Innovation Education and Research Vol. 9 No. 6, 2021, https://doi.org/10.31686/ijier.vol9.iss6.3165.

20“An Influx of Chinese Cars Is Terrifying the West,” Economist, accessed July 10, 2024, https://www.economist.com/leaders/2024/01/11/an-influx-of-chinese-cars-is-terrifying-the-west.

21Alexandra Scaggs, “Companies’ Confusing Cash Hoards,” Financial Times, November 16, 2023, https://www.ft.com/content/4d782ed1-5a1d-4576-9abe-c7b6d05bdc19.

22”Gross Savings (% of GDP),” World Bank Open Data, Accessed July 10, 2024, https://data.worldbank.org/indicator/NY.GNS.ICTR.ZS?end=2023&start=2000&view=chart.

23Michael Pettis, “Global Capital Is the Tail That Wags the U.S. Economic Dog,” Carnegie Endowment for International Peace, September 29, 2020, https://carnegieendowment.org/posts/2020/09/global-capital-is-the-tail-that-wags-the-us-economic-dog?lang=en.

24Robert Lawrence, “Recent Manufacturing Employment Growth: The Exception That Proves the Rule,” National Bureau of Economic Research, December 2017, https://doi.org/10.3386/w24151.

25“What Is the National Deficit?,” FiscalData, accessed July 10, 2024, https://fiscaldata.treasury.gov/americas-finance-guide/national-deficit/.

26“GDP Share by Industry U.S. 2023,” Statista, accessed July 10, 2024, https://www.statista.com/statistics/248004/percentage-added-to-the-us-gdp-by-industry/.

27Michael Pettis, “A (Very Short) History of Global Reserve Currencies,” Financial Times, June 7, 2023, https://www.ft.com/content/c967ba48-f21b-4222-9f11-beb61ce710ae.

28Barry Eichengreen, Globalizing Capital: A History of the International Monetary System (Princeton, NJ: Princeton University Press, 1996).

29“Maddison Project Database 2023,” University of Groningen, April 26, 2024, https://www.rug.nl/ggdc/historicaldevelopment/maddison/releases/maddison-project-database-2023.

30David Hume, “Of the Balance of Trade,” 1752. https://davidhume.org/texts/pld/bt.

31Barry Eichengreen and Marc Flandreau, “The Rise and Fall of the Dollar, or When Did the Dollar Replace Sterling as the Leading International Currency?,” National Bureau of Economic Research, July 2008, https://doi.org/10.3386/w14154.

32Eichengreen, Globalizing Capital.

33Barry Eichengreen, Golden Fetters: The Gold Standard and the Great Depression, 1919-1939 (Oxford: Oxford University Press, 1996).

34Michael Pettis, “The High Price of Dollar Dominance,” Foreign Affairs, June 30, 2023, https://www.foreignaffairs.com/united-states/high-price-dollar-dominance.

35Jane D’Arista, “The Evolving International Monetary System,” Cambridge Journal of Economics 33, no. 4 (2009): 633–52, https://doi.org/10.1093/cje/bep027.

36Peter M. Garber, “The Collapse of the Bretton Woods Fixed Exchange Rate System,” in A Retrospective on the Bretton Woods System: Lessons for International Monetary Reform, eds. Michael D. Bordo and Barry Eichengreen (Chicago, IL: University of Chicago Press, 1993), 461–94, https://www.nber.org/books-and-chapters/retrospective-bretton-woods-system-lessons-international-monetary-reform/collapse-bretton-woods-fixed-exchange-rate-system.

37Dev Patel, Justin Sandefur, and Arvind Subramanian, “A Requiem for Hyperglobalization,” Foreign Affairs, June 12, 2024, https://www.foreignaffairs.com/china/requiem-hyperglobalization.

38Michael Pettis, “Which Country Should Design U.S. Industrial Policy?,” Carnegie Endowment for International Peace, July 16, 2024, https://carnegieendowment.org/china-financial-markets/2024/07/which-country-should-design-us-industrial-policy?lang=en.

39Michael Pettis, “Changing the Top Global Currency Means Changing the Patterns of Global Trade,” Carnegie Endowment for International Peace, April 12, 2022, https://carnegieendowment.org/china-financial-markets/2022/04/changing-the-top-global-currency-means-changing-the-patterns-of-global-trade?lang=en.

40Pettis, “Which Country Should Design U.S. Industrial Policy?”

41“U.S. Senators Tammy Baldwin and Josh Hawley Lead Bipartisan Effort to Restore Competitiveness to U.S. Exports, Boost American Manufacturers and Farmers,” Office of U.S. Senator Tammy Baldwin for Wisconsin, July 31, 2019, https://www.baldwin.senate.gov/news/press-releases/competitive-dollar-for-jobs-and-prosperity-act.

42Michael W. Klein, with Kristin J. Forbes and Iván Werning (discussants), “Capital Controls: Gates versus Walls,” Brookings Institution, Fall 2012, https://www.brookings.edu/articles/capital-controls-gates-versus-walls/.

43Maurice Obstfeld, “The Dangers of a US Capital Inflow Tax,” Project Syndicate, June 14, 2024, https://www.project-syndicate.org/commentary/capital-inflow-tax-to-cut-us-trade-deficit-would-be-a-disaster-by-maurice-obstfeld-2024-06.

44Pettis, “Changing the Top Global Currency Means Changing the Patterns of Global Trade.”

45James Boughton, “Why White, Not Keynes? Inventing the Postwar International Monetary System,” International Monetary Fund, March 1, 2002, https://www.imf.org/en/Publications/WP/Issues/2016/12/30/Why-White-Not-Keynes-Inventing-the-Post-War-International-Monetary-System-15718; and Benn Steil, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order (Princeton, NJ: Princeton University Press, 2013). Keynes’ proposed bancor would be used to settle international accounts, and nations that are members of the International Clearing Union would pay a membership quota that is proportionate to their total trade. Thus, surplus countries would receive bancor credit, while deficit countries would have a negative account. Restrictions would be placed on each country’s bancor balance, to discourage surpluses and deficits. When these limits were breached, the currencies of surplus countries would be allowed to appreciate (and deficit countries, depreciate), stimulating a rebalancing of trade.